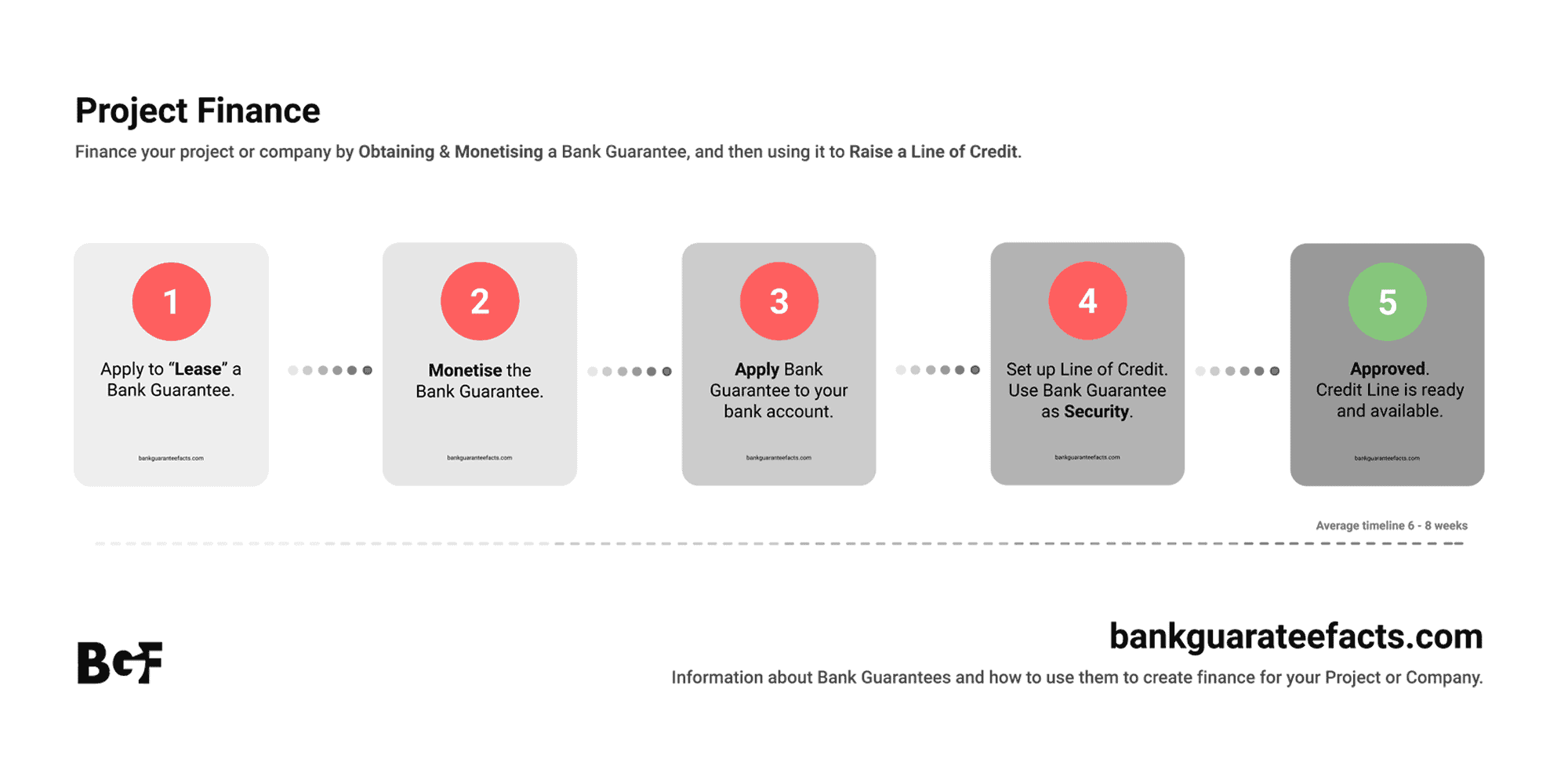

Monetising a Bank Guarantee

Key Facts

Monetising a Bank Guarantee.

The monetisation of a Demand Bank Guarantee is a form of asset based lending. The monetisation is subject to the (LVT) loan to value rate that was applied prior to receiving it. This means that a 10 million Euro BG with a 90% LTV can me used to raise a line of credit up to 9 million Euros.

We can make an

introduction

We can introduce you to boutique finance companies that specialise in delivering corporate funding.

Free document download

facility

We have a range of useful documents and information to assist you with gaining finance for your projector company.

We can answer your

questions

We answer your questions in relation to Bank Guarantees. Click here to get the answers you need to make an informed decision.

If a company wishes to Monetise a Bank Guarantee in order to receive a loan or credit line, referred to as Credit Guarantee Facilities, the wording must be specific to that of a Demand Bank Guarantee. Monetising a Bank Guarantee is governed by ICC Uniform Rules for Demand Guarantees, (URDG 758), and is used for monetising.

A Demand Bank Guarantee will allow the Beneficiary to confidently approach their bank, utilising the Bank Guarantee as security. This will allow them to apply for a capital injection, straight bank loan or a line of credit, referred to as Credit Guarantee Facilities.

The Beneficiary should negotiate the details of loan or a credit line with their bank or lender, such as the LTV (Loan to Value) prior to receiving the Bank Guarantee on their account, confirming the wording of the Bank Guarantee is acceptable. The LTV value is important as it defines the maximum value of the line of credit that can be raised against it. We have a demand bank guarantee calculator to help define the value of bank guarantee required to rais the line of credit you require.

If you would like further information, or to speak with an expert, please visit our contact page.

If you have any further questions on this or any other subject related to bank guarantees, then you can search our frequently asked questions where you will hopefully find the answer you are looking for. Alternatively you can ask us a question and we will answer it for you.

Bank Guarantee is applied to the Beneficiarys bank account.

Application to bank for a Line of Credit, with Bank Guarantee as Security.

Application Approved by bank and Credit Line is ready and available.

{kind=link}